ASX 200 Inches Higher as Healthcare and Tech Rally Offset Ex-Dividend Drag

Team Skrill Network

Team Skrill Network comprises seasoned professionals from diverse fields including Finance, Mining, Technology, Investing, and Digital Strategy. They bring a deep knowledge and understanding of financial markets and behavioural patterns to every story, ensuring credibility and precision in every piece. Whether analysing emerging market trends or spotlighting small- and mid-cap growth companies across ASX, TSX, or NASDAQ, the team’s editorial approach blends data-driven insights with compelling storytelling. Their expertise enables them to process complex developments into content that resonates with both institutional investors and retail audiences. Backed by experience in content curation, SEO strategy, and investor-focused messaging, the team of writers at Skrill Network are committed to delivering stories that matter—authentic, relevant, and strategically aligned with the evolving landscape of global investing.

Read more

Key Highlights

- ASX 200 rose 0.19% to 8,780.4 points despite a cautious global backdrop.

- Healthcare and technology stocks led gains, with Neuren Pharmaceuticals soaring nearly 30% on positive European regulatory news.

- Oil prices firmed after renewed US-Iran tensions, while iron ore edged higher and gold slipped.

- Property and infrastructure stocks weighed on the index as several heavyweight companies traded ex-dividend.

- Markets are preparing for a busy week of economic data, including RBA minutes, Chinese PMI figures and US jobs data.

The Australian share market edged higher on Monday, shaking off another cautious lead from Wall Street as investors returned to healthcare and technology stocks while navigating fresh geopolitical tensions in the Middle East and the final trading days of the financial year.

By midday, the S&P/ASX 200 had gained 0.19% to 8,780.4 points, while the broader All Ordinaries rose 0.22% to 8,983.7. Small caps also outperformed, with the Small Ordinaries Index climbing 0.53%, suggesting investors were still willing to take selective risk despite heightened global uncertainty.

The strongest momentum came from technology and healthcare, helping offset weakness across property, industrials and utilities, where several large companies traded ex-dividend and mechanically declined.

Market Snapshot

Global markets remain cautious

Australian equities outperformed most regional markets after Wall Street ended Friday on a softer note. The Dow Jones slipped 0.09%, the S&P 500 eased 0.05% and the Nasdaq lost 0.24% as investors continued to rotate away from richly valued technology stocks ahead of another busy earnings season.

Across Asia, sentiment remained mixed. Japan’s Nikkei fell 0.9%, South Korea’s Kospi declined 1.2% and Shanghai eased 0.1%, while Hong Kong’s Hang Seng gained 0.7%.

Markets also kept one eye on developments in the Middle East after renewed missile exchanges between US and Iranian forces briefly raised concerns about oil supplies through the Strait of Hormuz. Those fears eased after reports that both nations had agreed to resume diplomatic talks in Qatar later this week, although traders remained cautious.

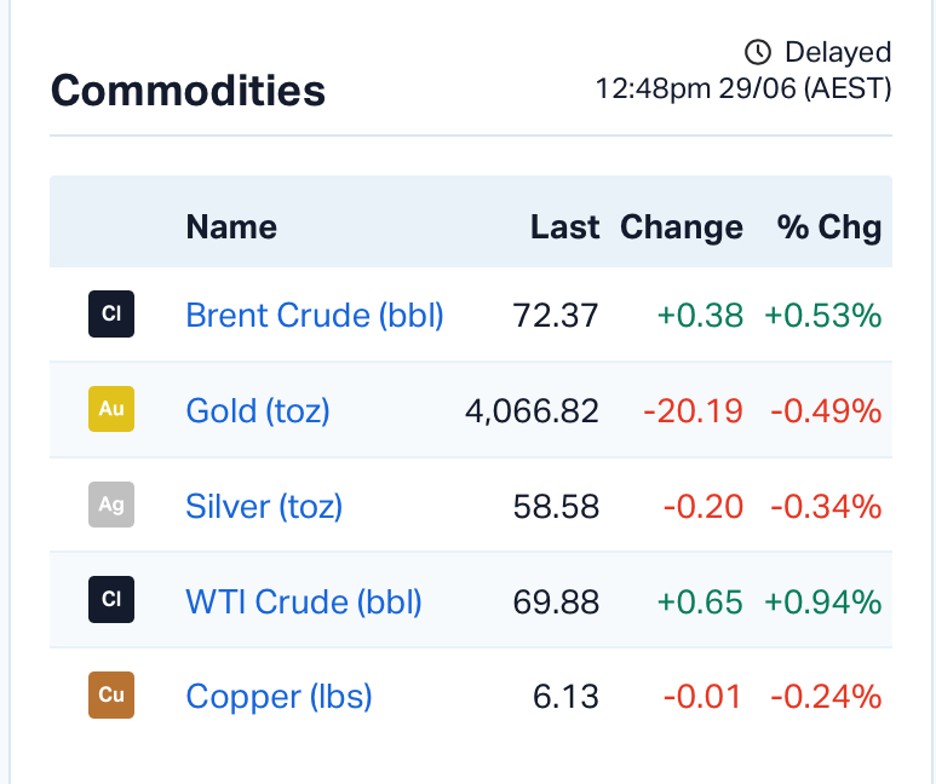

Brent crude rose 0.53% to US$72.37 a barrel, while West Texas Intermediate gained 0.94% to US$69.88. Gold slipped 0.49% to US$4,066.82 an ounce as some investors shifted back toward risk assets, while iron ore climbed 1% to US$98.50 a tonne.

Commodities Price Index | Source: MarketIndex

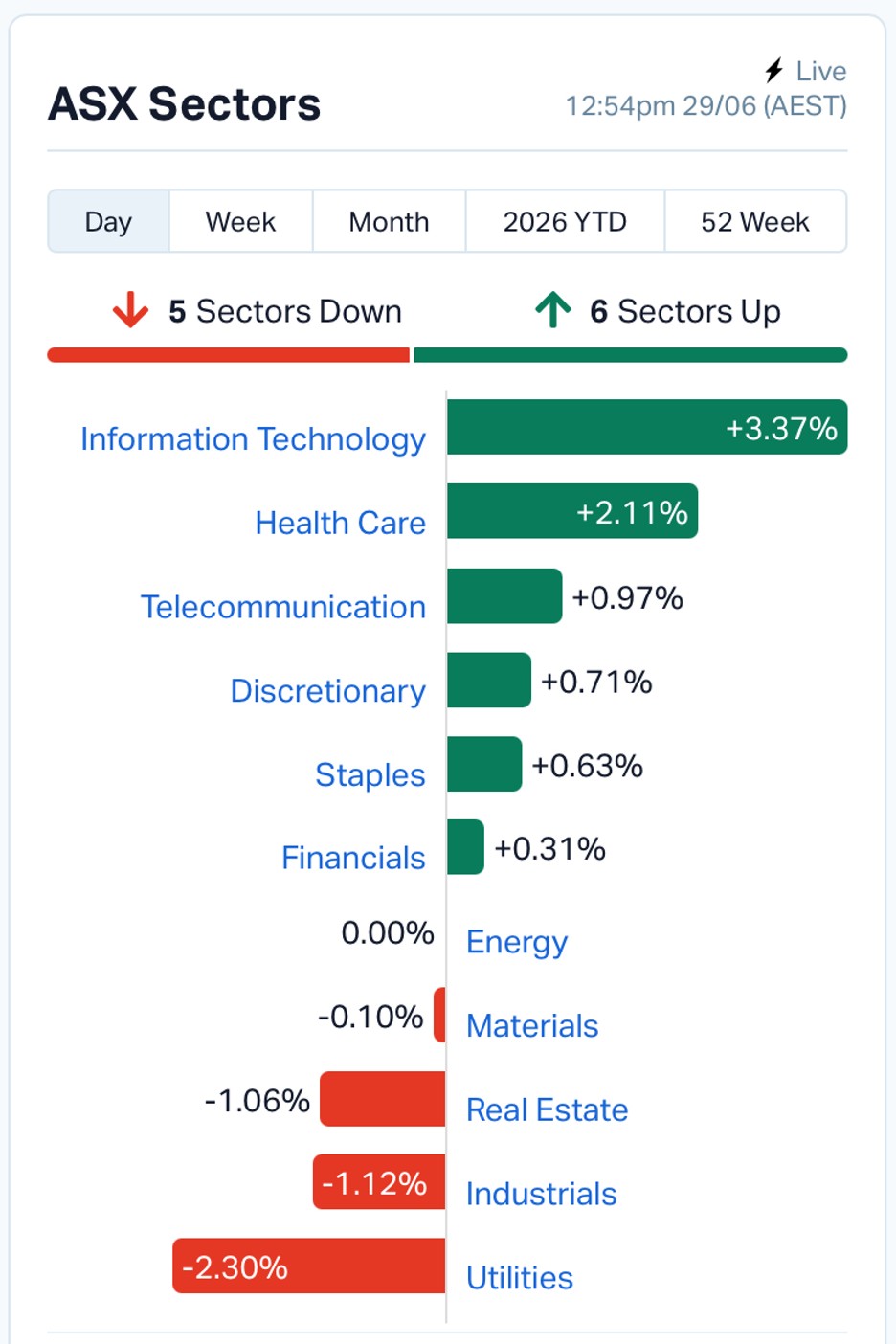

Technology and healthcare take the lead

The ASX All Technology Index jumped 3.08%, making it the day’s strongest performing sector despite continued volatility in US technology shares.

ASX 200 Sector Snapshot | Source: MarketIndex

Healthcare followed with a 2.11% gain as investors responded to encouraging regulatory developments.

Neuren Pharmaceuticals (ASX: NEU) surged 29.5% after announcing that the European Medicines Agency’s Committee for Medicinal Products for Human Use adopted a positive opinion recommending approval of its Rett syndrome treatment, DAYBUE. If formally approved by the European Commission, the therapy would become the first treatment of its kind available across Europe. Under its licensing agreement, Neuren could receive an immediate US$35 million milestone payment following the first commercial sale, with up to US$170 million in additional sales milestones.

Technology stocks also attracted fresh buying. Life360 climbed 10.8%, while enterprise software company Nuix gained more than 10% as traders returned to high-growth technology names following last week’s profit taking.

Financials edged 0.31% higher, supported by insurers, although Judo Capital remained under pressure after last week’s earnings downgrade.

Ex-dividend season weighs on property stocks

The biggest drag on Monday’s session came from real estate and infrastructure stocks rather than deteriorating company fundamentals.

Several large property groups, including Stockland, Goodman Group, Mirvac, Dexus, Charter Hall and Centuria, traded ex-dividend, automatically reducing their share prices by the value of the upcoming dividend.

Stockland fell 5.79%, APA Group dropped 4.46% and Transurban declined 4.55%, making them among the weakest performers on the benchmark index.

Materials also softened by 1.06%, although stronger iron ore prices helped limit losses among the major miners.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

Macro factors remain firmly in focus

Away from company earnings, investors continued to assess several important economic developments.

Reserve Bank Assistant Governor Christopher Kent unveiled a new framework outlining how the central bank could deploy additional monetary policy tools during future periods of exceptionally low interest rates. While the cash rate remains the RBA’s primary policy instrument, the updated framework includes options such as bond purchases, forward guidance, yield targeting, negative interest rates and foreign asset purchases if extraordinary circumstances require further stimulus.

Currency markets also remained under pressure. The Australian dollar slipped to US68.91 cents after Commonwealth Bank currency strategist Joseph Capurso warned the local currency could remain under pressure as expectations for further RBA rate increases continue to fade.

Capurso also noted that increasing global investment in artificial intelligence and advanced technology could see Australia increasingly viewed as an “old economy”, creating further headwinds for the Australian dollar.

Meanwhile, the Australian Competition and Consumer Commission warned fuel retailers against using this week’s partial restoration of the fuel excise to unfairly increase prices. From July 1, the fuel excise discount will reduce from 32 cents per litre to 16 cents per litre.

Looking ahead

Investors now turn their attention to a busy week of economic data that could shape market sentiment heading into July. The release of the RBA’s latest meeting minutes, Chinese manufacturing PMI figures, Australia’s home price index and trade data, along with US non-farm payrolls later in the week, are expected to provide fresh clues on the direction of interest rates and global economic growth.

For now, Monday’s session suggests the Australian market remains resilient. While geopolitical risks and global macro uncertainty continue to dominate headlines, strong buying in healthcare and technology has helped keep the benchmark index in positive territory as the financial year draws to a close.

Source: ASX, Markets Live Data, Reserve Bank of Australia, Commonwealth Bank, ACCC, Reuters.

What is your take on this story?

This is user sentiment & not financial advice.

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.