ASX Falls Again As Global Tech Cools And AI Spending Surge Keeps Rate Jitters Alive

Team Skrill Network

Team Skrill Network comprises seasoned professionals from diverse fields including Finance, Mining, Technology, Investing, and Digital Strategy. They bring a deep knowledge and understanding of financial markets and behavioural patterns to every story, ensuring credibility and precision in every piece. Whether analysing emerging market trends or spotlighting small- and mid-cap growth companies across ASX, TSX, or NASDAQ, the team’s editorial approach blends data-driven insights with compelling storytelling. Their expertise enables them to process complex developments into content that resonates with both institutional investors and retail audiences. Backed by experience in content curation, SEO strategy, and investor-focused messaging, the team of writers at Skrill Network are committed to delivering stories that matter—authentic, relevant, and strategically aligned with the evolving landscape of global investing.

Read more

Key Highlights

- ASX 200 drops 1.33 percent as tech and materials weigh on the index

- Wall Street extends its losing streak, with US indices lower again overnight

- Amazon launches a 15 billion US dollar bond deal to fuel AI infrastructure spending

- Australian banks and rate expectations remain in focus after comments from CBA’s chief executive

- Health care is the only ASX sector in positive territory as investors tilt toward defensive names

ASX sinks as global tech wobbles and AI funding boom meets rate nerves

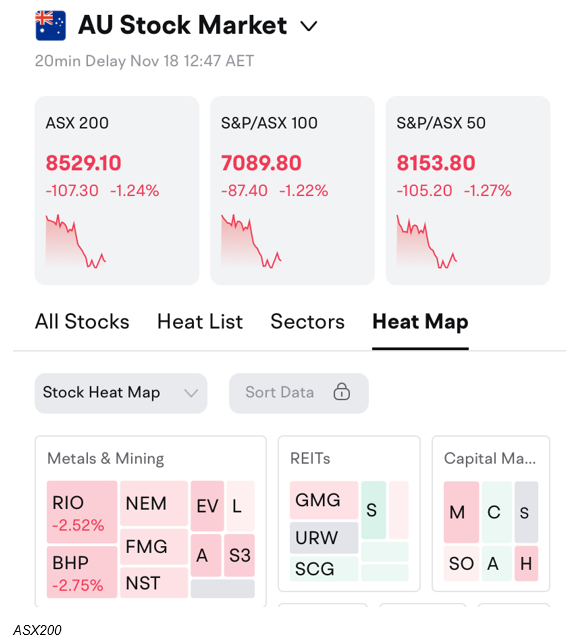

Australian shares extended their recent slide on Tuesday, with the S&P ASX 200 falling 1.33 percent to 8,521.6 by midday as investors reacted to another risk off session on Wall Street and ongoing uncertainty around the rate outlook at home. The broader All Ordinaries index slipped 1.36 percent to 8,794.3.

Selling was broad based, with ten of the eleven sectors in the red and only health care managing to eke out a modest gain. Technology and materials names took the heaviest hit, reflecting both global growth jitters and pressure on higher valuation stocks.

Local sentiment was also tested by remarks from Commonwealth Bank chief executive Matt Comyn at a parliamentary hearing, where he described it as “unlikely” that interest rates will move in the near term, including any cuts in 2026. The comments reinforced the view that borrowers may face a longer period of restrictive settings, while CBA shares traded around 2 percent lower during the session.

Market Snapshot

Wall Street weakens again as AI boom meets valuation fatigue

Overnight, US equities posted another down day. The Dow Jones Industrial Average fell 1.18 percent to 46,590 points, the S&P 500 slipped 0.92 percent to 6,672 and the Nasdaq eased 0.84 percent to 22,708. It was the latest sign that the powerful rally in large technology and growth names is pausing as investors weigh stretched valuations against a still uncertain rate path.

Under the surface, a more complex story is playing out. On one hand, major technology groups are committing to massive spending on data centres and artificial intelligence infrastructure. On the other, bond markets and central bank signals are reminding investors that money is not free.

A key example overnight came from Amazon. The e commerce and cloud giant launched its first US dollar bond sale in three years, seeking to raise 15 billion US dollars through a six tranche deal. Investor demand reportedly peaked at around 80 billion US dollars in orders, allowing the company to tighten pricing on the longest dated portion.

S&P500 Heatmap | Source: TradingView

Proceeds from the bond are earmarked for a range of purposes, including capital expenditure and acquisitions, and come at a time when analysts estimate that major platforms such as Amazon, Meta and Alphabet could collectively spend about 400 billion US dollars on AI linked infrastructure this year. Meta recently announced a large bond program of its own, while Oracle has also been flagged as a likely issuer.

The funding spree highlights an important tension that equity markets are trying to reconcile. AI and digital infrastructure are seen as long term growth engines, yet they require heavy upfront investment in a world where borrowing costs remain elevated. That is one reason why rate expectations and inflation trends continue to matter for tech valuations, even when earnings headlines look positive.

Macro backdrop: rates, banks and household pressure

Back in Australia, the macro conversation was dominated by the House of Representatives economics committee hearing, where CBA’s Matt Comyn fielded questions on profitability, fees and the bank’s use of AI in lending and fraud prevention. Comyn reiterated that the bank is seeing strong customer engagement with digital and AI enabled tools, but also acknowledged that households are feeling the pressure of higher costs.

The discussion came against a backdrop of ongoing debate about whether banks are doing enough for lower income customers, after an earlier review by ASIC highlighted high fees for some vulnerable groups. While this does not create an immediate market shock, it adds to the list of factors investors must assess when valuing the financial sector, from regulatory risk through to growth in fee based businesses.

On the rates front, traders are still pricing in the possibility of cuts further out, but the tone from central bankers globally has been careful rather than dovish. That aligns with comments from market strategists who argue that an expensive equity market typically needs clear visibility on lower rates or strong earnings upgrades to sustain current multiples.

Sector moves: tech and resources lead declines

The selling on Tuesday was widespread.

- The All Technology Index fell 3.59 percent to 3,505.3 as investors unwound positions in high beta names in sympathy with US tech weakness.

- Materials slumped 5.88 percent, reflecting concerns around global demand and further pressure on some metals linked to China’s growth outlook.

- Financials dropped 1.93 percent, while energy, telecommunications and discretionary names also finished lower.

- Health care was the only sector in positive territory, edging up 0.24 percent as investors sought defensive earnings and balance sheet strength.

Gold producers did not escape the sell off despite relatively small moves in the underlying metal price. The ASX All Ordinaries Gold Index fell 2.07 percent even as spot gold eased only 0.15 percent to about 4,040 US dollars per ounce.

Top movers: James Hardie shines, tech and silver names struggle

Among the top gainers, building materials group James Hardie Industries (JHX) stood out with a 6.57 percent rise to $27.10. Analysts at RBC Capital Markets highlighted that the company’s latest quarterly update and guidance upgrade signal improving cost control, better utilisation across plants and more robust earnings visibility. The broker pointed to early wins with customers, synergy benefits and a stronger forecasting framework as reasons for optimism.

Other notable risers included:

- Meteoric Resources (MEI) up 5.71 percent

- Liontown Resources (LTR) up 4.11 percent

- IGO (IGO) and Pilbara Minerals (PLS), both recovering modestly after recent volatility in the lithium complex

On the downside, the worst performers were concentrated in smaller resources and technology names:

- Unico Silver (USL) fell 23.33 percent to $0.5175

- European Lithium (EUR) dropped 15 percent

- Technology One (TNE) slid 14.49 percent

- Artrya (AYA), Superloop (SLC), Aussie Broadband (ABB) and Catapult Sports (CAT) also posted declines of between 6 and 11 percent

The pattern reinforces the view that markets are punishing valuation outliers and companies with less certain cash flow profiles more harshly during this phase of consolidation.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

Commodities, FX and volatility

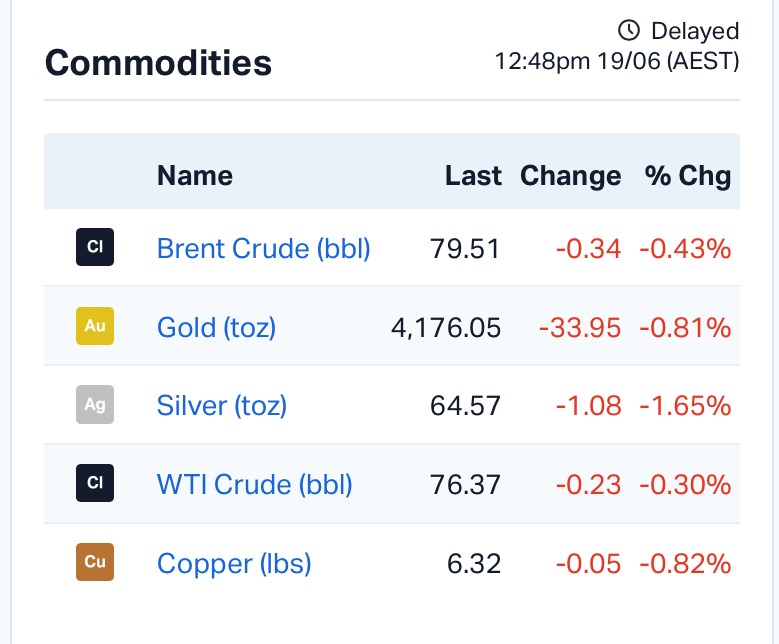

Commodity markets were relatively quiet compared with equities. Brent crude ticked lower to 63.91 US dollars a barrel, while WTI crude slipped to 59.60 US dollars. Copper traded close to flat near 4.98 US dollars per pound, suggesting that while growth worries are present, they are not yet signalling a sharp downturn in industrial activity.

The Australian dollar softened slightly to about 64.85 US cents, with modest declines against the euro, pound and Canadian dollar. Foreign exchange traders are watching both US rate expectations and any sign that Chinese demand indicators move decisively in either direction.

The S&P ASX 200 Volatility Index sits around 13.6, still within the low range that historically corresponds with cautious consolidation rather than panic selling. That supports the idea that markets are in a repricing phase after a strong run, rather than a full blown risk capitulation.

What the experts are watching next

Market strategists say the next leg for equities will depend on three key threads.

First is the interplay between the AI funding boom and bond markets. The Amazon bond sale, alongside earlier issues from other mega caps, shows that demand for high quality corporate credit remains solid, but it also underscores how much capital will be needed for AI infrastructure in a world of higher rates.

Second is earnings quality. Analysts are scrutinising guidance for 2026 and beyond, with a preference for companies that can grow margins without relying too heavily on financial engineering or one off cost cuts.

Third is domestic policy and household resilience. With the largest banks signalling no early relief on borrowing costs, investors are watching consumer exposed sectors closely for signs of stress or adaptation.

For now, the ASX is trading in step with global markets that are digesting a mix of strong long term themes and shorter term valuation questions. It is a reminder that even in a world excited by AI and digital transformation, the basic disciplines of price, cash flow and balance sheets still matter.

What is your take on this story?

This is user sentiment & not financial advice.

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.