ASX Surges 1.7% as Miners Rally on Peace Hopes, Energy Stocks Lag

Key Highlights:

- S&P/ASX 200 jumps 1.7% to 8,625.9

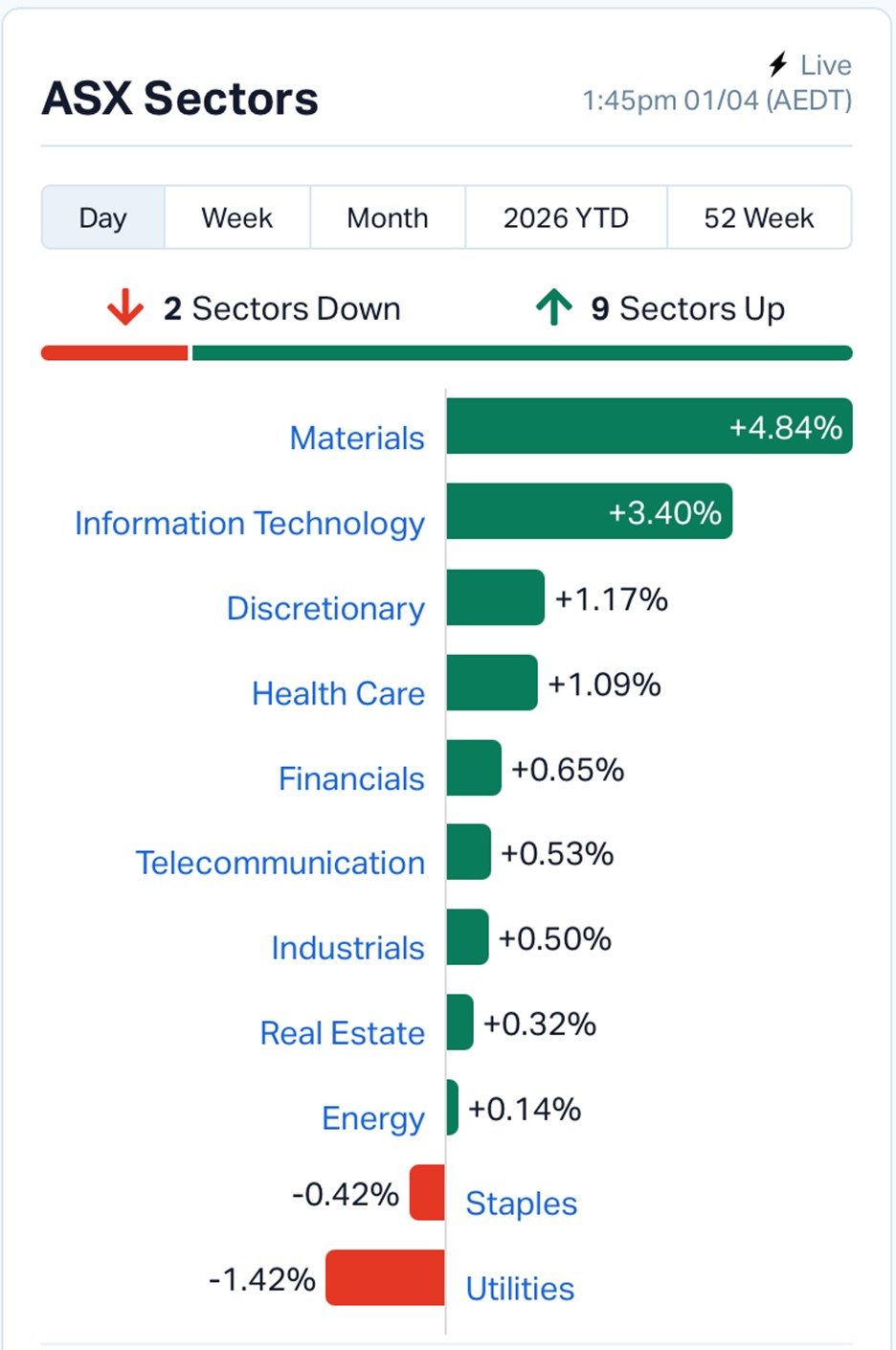

- Materials sector leads with +4.91%, driven by miners and metals

- Tech stocks rebound strongly, lifting the ASX All Technology Index +3.03%

- Energy and utilities decline as oil outlook softens

- Wall Street rally fuels global risk-on sentiment

The Australian share market has staged one of its strongest sessions in weeks, riding a wave of global optimism as easing geopolitical tensions shift investor sentiment back toward risk.

By early afternoon, the S&P/ASX 200 was up 1.7% to 8,625.9, with broad-based gains across most sectors. The rally comes after a sharp rebound on Wall Street overnight, where US markets surged on hopes that tensions in the Middle East may begin to de-escalate.

Sector Snapshot | Source: MarketIndex

A Market Rebound Built on Hope

Overnight, US benchmarks posted strong gains, with the S&P 500 rising nearly 3% and the Nasdaq jumping close to 4%.

The trigger was renewed optimism that US involvement in the Iran conflict could wind down within weeks, reducing the risk of a prolonged energy crisis.

For markets, this matters.

Geopolitical tensions tend to push oil prices higher, squeeze global growth, and weigh on equities. The mere suggestion of an easing conflict has been enough to unwind some of that fear.

The result is a classic “risk-on” rally, where investors rotate back into growth and cyclical sectors.

Miners Take the Lead

The biggest beneficiaries of this shift were mining stocks.

The materials sector surged 4.91%, making it the standout performer on the day. Resource-heavy indices also reflected the strength, with the ASX 200 Resources index climbing more than 4%.

Gold and lithium names saw aggressive buying, with stocks like Benz Mining and European Lithium posting double-digit gains.

This may seem counterintuitive at first. Gold is typically a safe haven, while lithium is tied to growth.

But in today’s market, both are benefiting from different narratives.

Gold continues to hold firm amid lingering uncertainty, while lithium and base metals are riding expectations of stabilising global trade and demand.

The underlying theme is clear. Investors are positioning for a world where the worst-case energy shock may not materialise.

Tech Joins the Party

Technology stocks also joined the rally, with the ASX All Technology Index rising 3.03%.

Names like Zip Co Ltd surged over 10%, reflecting renewed appetite for growth stocks.

This follows the global trend seen overnight, where US tech giants led the rebound.

After a volatile March, investors appear willing to re-enter the sector, particularly as bond yields stabilise and risk sentiment improves.

The Energy Sector Stands Apart

Interestingly, not every sector participated in the rally.

Energy stocks slipped 0.28%, making them one of the few laggards.

The reason is simple.

If geopolitical tensions ease, oil prices are expected to stabilise or even decline. That reduces the windfall profits energy companies had been enjoying during the recent spike.

Utilities also fell 1.40%, as investors rotated out of defensive plays and into higher-growth opportunities.

This divergence highlights a broader shift in market positioning.

Investors are moving away from “protection trades” and back into sectors tied to economic expansion.

A Market Driven by Mechanics

While the headlines point to geopolitics, part of the rally may also be technical.

March marked a difficult month for global equities, with significant losses across major indices.

As the quarter ended, fund managers were forced to rebalance portfolios, increasing exposure to equities to maintain target allocations.

This created additional buying pressure, amplifying the upward move.

Analysts note that such flows can accelerate rallies, even when underlying fundamentals remain uncertain.

Corporate Movers: Winners and Losers

Among individual stocks, HMC Capital Ltd led the gains, jumping more than 15%.

Mining and resource names dominated the top performers list, reinforcing the strength in the materials sector.

On the downside, Pexa Group Ltd fell sharply by over 16%, making it the session’s biggest decliner.

Energy-related stocks also featured among the laggards, reflecting the sector-wide pullback.

The Global Backdrop

The ASX rally did not occur in isolation.

Globally, markets are attempting to stabilise after a period of heightened volatility.

In the US, strong gains were partly driven by short covering and hedging activity following a weak month.

In Asia, however, the picture remains mixed, with Japanese and Chinese markets showing signs of caution.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

Commodities are also sending mixed signals.

Gold continues to edge higher, trading near record levels above $US4,690 per ounce, suggesting that some investors remain wary.

Meanwhile, Brent crude is hovering around $US105 per barrel, still elevated but no longer accelerating.

Commodities Snapshot | Source: MarketIndex

The Bigger Picture: A Fragile Recovery

Today’s rally tells a compelling story, but it is not without caveats.

At its core, the market is responding to expectations rather than confirmed outcomes.

Peace in the Middle East remains uncertain. Inflation pressures persist. And central banks, including the Reserve Bank of Australia, are still navigating a complex balancing act.

What the market is doing is pricing in a best-case scenario.

That includes:

- A de-escalation of geopolitical tensions

- Stabilising energy prices

- Continued economic resilience

If any of these assumptions falter, volatility could return quickly.

What to Watch Next

Investors will now turn their attention to upcoming economic data and central bank signals.

In particular, any confirmation of easing tensions in the Middle East will be critical in sustaining the current rally.

Locally, the focus remains on inflation trends and consumer resilience, especially after recent data showed pressure on household budgets.

For now, the market is enjoying a moment of relief.

But as history often shows, relief rallies can be powerful yet short-lived if not supported by fundamentals.

What is your take on this story?

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.