Boss Energy (ASX: BOE) Builds 45Mlb Uranium War Chest, Extending Honeymoon’s Lifeline

Team Skrill Network

Team Skrill Network comprises seasoned professionals from diverse fields including Finance, Mining, Technology, Investing, and Digital Strategy. They bring a deep knowledge and understanding of financial markets and behavioural patterns to every story, ensuring credibility and precision in every piece. Whether analysing emerging market trends or spotlighting small- and mid-cap growth companies across ASX, TSX, or NASDAQ, the team’s editorial approach blends data-driven insights with compelling storytelling. Their expertise enables them to process complex developments into content that resonates with both institutional investors and retail audiences. Backed by experience in content curation, SEO strategy, and investor-focused messaging, the team of writers at Skrill Network are committed to delivering stories that matter—authentic, relevant, and strategically aligned with the evolving landscape of global investing.

Read more.webp&w=3840&q=75)

Key Highlights

- Boss Energy expands uranium inventory to 45+ million pounds across satellite deposits

- Gould’s Dam resource jumps 30% to 33.1Mlbs, Jason’s rises to 12.0Mlbs

- Low-cost expansion strategy leverages existing Honeymoon infrastructure

- Mining lease applications targeted H2 2026, production pathway now defined

- Shares trade at $1.535, down 5.83%, reflecting broader uranium market softness

A quiet build into a long-term uranium powerhouse

While global energy markets continue to swing between volatility and uncertainty, Boss Energy appears to be playing a longer game.

In a detailed update to the ASX, the company revealed a significant upgrade to its uranium resources at Gould’s Dam and Jason’s Deposit, effectively assembling a 45 million pound uranium “war chest” in close proximity to its producing Honeymoon operation in South Australia.

This is not just another resource update. It signals a structural shift in how Boss is positioning itself, from a single-asset producer into a multi-deposit uranium hub with decades of potential supply.

Market Snapshot

The numbers behind the narrative

The headline figures are substantial.

Gould’s Dam now hosts 33.1 million pounds of uranium, up 30% from previous estimates, while Jason’s Deposit contributes another 12.0 million pounds, taking the combined satellite inventory beyond 45 million pounds.

The increase is largely driven by additional drilling and improved geological modelling, particularly using advanced tools like PFN logging and permeability mapping. While average grades declined, a common outcome in resource expansions, the broader mineralised footprint has grown significantly.

In mining terms, this is a classic trade-off. Lower grades, but larger, more continuous deposits that are easier and cheaper to extract.

Why this matters: It’s not just about size

What makes this update compelling is not just the scale, but the economics and strategy behind it.

Both deposits are suited to in-situ recovery (ISR), a mining method that avoids traditional open pits or underground operations. Instead, uranium is dissolved underground and pumped to the surface. This dramatically reduces capital costs and environmental footprint.

Boss is already applying this method at Honeymoon, and importantly, it plans to replicate the same approach across these satellite deposits.

Managing Director Matthew Dusci explained:

“The updated Mineral Resource Estimates… highlight the significance of these deposits, with Gould’s Dam and Jason’s Deposit hosting 33Mlbs and 12Mlbs of uranium respectively, with mineralisation at both deposits remaining open.”

He added that ongoing work is focused on fast-tracking development:

“The Company has been progressing ecological, groundwater and radiological baseline surveys together with preliminary technical studies… targeting submission of Mining Lease applications during the second half of this calendar year.”

A low-cost expansion model taking shape

The real strategic advantage lies in infrastructure leverage.

Jason’s Deposit sits just 13km from Honeymoon. Boss plans to connect it via a “trunk line” system, effectively piping uranium-bearing solution directly to the existing plant. No new processing facility required.

Gould’s Dam, located 80km away, may require a satellite facility, but still benefits from shared expertise and processing frameworks.

This hub-and-spoke model mirrors strategies used by major uranium players globally, including operations in Kazakhstan and parts of the United States, where ISR mining dominates.

The 2026–2029 pathway investors will watch

The next phase is now clearly mapped.

Boss aims to submit mining lease applications in the second half of 2026. Based on current timelines, approvals could take 18 to 24 months, followed by environmental clearances.

A Pre-Feasibility Study is expected by Q3 2027, which will be a critical milestone in translating these resources into economic production.

If timelines hold, development could begin before the end of the decade.

Industry context: A tightening uranium market

This expansion comes at a time when uranium is regaining global relevance.

Governments across the US, Europe, and Asia are increasingly backing nuclear energy as a reliable, carbon-free baseload power source. Supply, however, remains constrained after years of underinvestment following the Fukushima downturn.

According to World Nuclear Association data, global uranium demand is expected to rise steadily through 2030, while new supply remains limited.

Against this backdrop, companies that can secure long-term, low-cost production pipelines are likely to hold a strategic advantage.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

Boss appears to be positioning itself squarely in that category.

Market reaction and stock snapshot

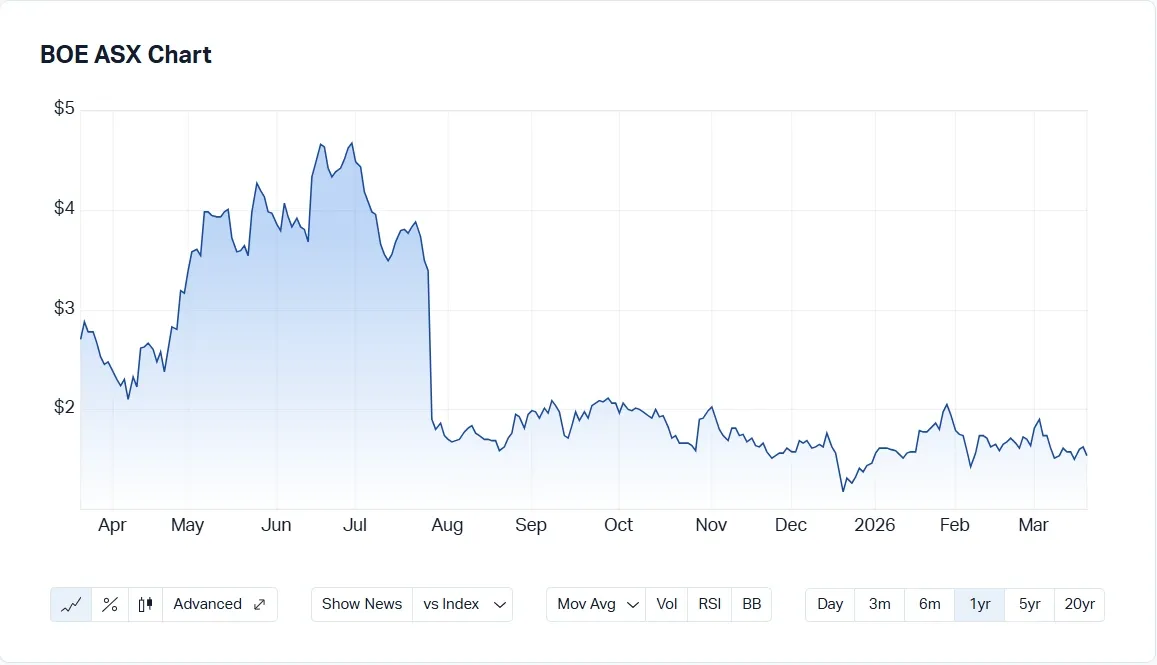

Despite the strong operational update, Boss Energy shares were trading at $1.535, down 5.83% on the day, with a market cap of approximately $637 million.

BOE 1-Year Stock Price Chart | Source: MarketIndex

The stock is down over 38% over the past year, reflecting broader weakness in uranium equities rather than company-specific fundamentals.

For context, the stock remains well below its 52-week high of $4.75.

The bigger picture: From miner to infrastructure play

What emerges from this update is a broader shift in identity.

Boss Energy is no longer just extracting uranium from a single deposit. It is building a regional uranium production network, anchored by Honeymoon and supported by satellite resources.

With over 45 million pounds now defined in its immediate vicinity, the company has effectively laid the groundwork for multi-decade production visibility.

In a world increasingly focused on energy security and decarbonisation, that kind of positioning is hard to ignore.

Boss Energy ASX Announcement, Market Data, March 19, 2026

What is your take on this story?

This is user sentiment & not financial advice.

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.