Cash Flow King: Sovereign Metals Unveils US$476M EBITDA Potential in Landmark Kasiya DFS

Team Skrill Network

Team Skrill Network comprises seasoned professionals from diverse fields including Finance, Mining, Technology, Investing, and Digital Strategy. They bring a deep knowledge and understanding of financial markets and behavioural patterns to every story, ensuring credibility and precision in every piece. Whether analysing emerging market trends or spotlighting small- and mid-cap growth companies across ASX, TSX, or NASDAQ, the team’s editorial approach blends data-driven insights with compelling storytelling. Their expertise enables them to process complex developments into content that resonates with both institutional investors and retail audiences. Backed by experience in content curation, SEO strategy, and investor-focused messaging, the team of writers at Skrill Network are committed to delivering stories that matter—authentic, relevant, and strategically aligned with the evolving landscape of global investing.

Read more

Key Highlights

- DFS confirms US$476M annual EBITDA and US$2.2B project valuation

- Positioned as world’s largest rutile and graphite producer

- Lowest-cost graphite globally, undercutting China

- Strategic backing from Rio Tinto and global offtake partners

- Zero tailings design and hydropower add ESG edge

Sovereign Metals has stepped into the spotlight after unveiling a definitive feasibility study that positions its Kasiya project as one of the most financially compelling critical minerals assets on the ASX.

The company is forecasting annual EBITDA of US$476 million and total revenue of US$16.2 billion over a 25-year mine life, placing it firmly in what analysts often call “tier-one” territory.

At a time when global markets are searching for reliable supply of strategic minerals, the scale and economics of Kasiya are hard to ignore.

Market Snapshot

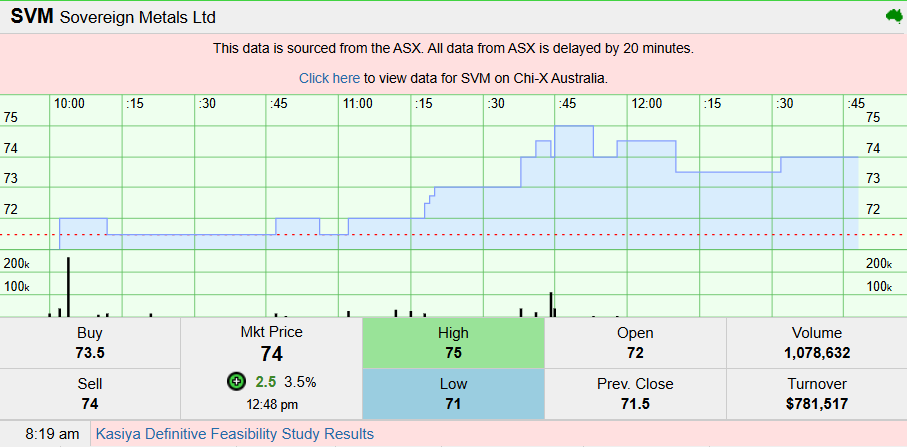

At the time of writing this article. SVM shares were up by 3.5% trading at A $0.74.

A Rare Combination of Scale and Simplicity

The Kasiya Rutile-Graphite Project in Malawi is not just large. It is structurally different.

Unlike many hard rock mining projects, Kasiya’s orebody is soft and free-dig. That means no drilling, blasting, or crushing is required, significantly lowering costs and operational risk.

The result is an operating cost of just US$450 per tonne, supporting strong margins even through commodity cycles.

At steady state, the project is expected to produce 222,000 tonnes of rutile and 275,000 tonnes of graphite annually, positioning Sovereign Metals Limited as a potential global leader in both markets.

A Financial Profile That Stands Out

The headline numbers tell a compelling story.

A pre-tax net present value of US$2.2 billion and an internal rate of return of 23% suggest a project that is not only profitable but resilient.

The NPV to capex ratio of 3.0x is particularly notable. In mining terms, that signals strong capital efficiency, especially for a project requiring US$727 million in initial investment.

Annual free cash flow is estimated at US$452 million, reinforcing the “cash flow king” narrative.

These metrics place Kasiya alongside some of the most attractive undeveloped projects globally, particularly in the critical minerals space.

A Strategic Answer to Global Supply Risks

Beyond financials, the project’s real strength lies in its strategic positioning.

Both rutile and graphite are classified as critical minerals by the United States and the European Union. These materials are essential for aerospace, defence, and battery technologies.

The United States currently produces no titanium sponge domestically and remains fully dependent on imports, according to US Geological Survey data. At the same time, China controls roughly 70% of global titanium production and around 77% of graphite supply.

Kasiya offers an alternative.

It is positioned as a large-scale, Western-aligned supply source at a time when governments are actively seeking to diversify away from China.

This dynamic has already attracted interest from global players.

Partnerships Add Credibility

The project is backed by Rio Tinto, which holds an 18.5% stake and provides technical oversight through a joint committee.

That involvement is significant.

Rio Tinto’s participation signals confidence in both the geology and execution pathway, reducing perceived development risk.

On the commercial side, non-binding offtake agreements cover more than half of initial rutile production and a substantial portion of graphite output, with partners including Mitsui and Traxys.

This early demand visibility is often a key hurdle for pre-production miners, and Kasiya appears to have cleared it.

Lowest-Cost Graphite, Globally

One of the more striking aspects of the study is graphite economics.

Kasiya’s graphite production cost is estimated at just US$216 per tonne, making it the lowest-cost producer globally based on publicly disclosed data.

That undercuts even Chinese producers, which typically operate around US$288 per tonne, according to Benchmark Minerals Intelligence.

In an industry where cost leadership often determines long-term survival, this positions Sovereign strongly.

It also provides a buffer against price volatility in battery materials markets.

ESG and Infrastructure Edge

The project also carries a strong environmental narrative.

Instead of a traditional tailings dam, Kasiya will use in-pit backfilling, reducing environmental risk and footprint.

Power will be sourced from Malawi’s hydropower grid, lowering emissions compared to fossil-fuel-based operations.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

Perhaps most striking is the rehabilitation outcome.

Pilot trials showed that mined land could be restored to agricultural use, with maize yields reaching 5.2 tonnes per hectare, more than five times the local average.

This is a rare example of mining and agriculture coexisting productively.

A Hidden Third Revenue Stream

Beyond rutile and graphite, there is additional upside.

The project is also recovering monazite, which contains heavy rare earth elements such as dysprosium, terbium, and yttrium.

These materials are critical for advanced electronics and defence technologies and are currently subject to Chinese export restrictions.

While not yet included in the DFS economics, this could emerge as a third revenue stream with minimal additional cost.

CEO Perspective

Managing Director and CEO Frank Eagar described the milestone in clear terms.

He said, “The completion of this DFS marks a defining milestone for Kasiya and for the global titanium and graphite supply chains. To deliver a DFS of this quality, depth and confidence, rarely achieved by a pre-production company, reflects the calibre of partnerships that Sovereign has assembled around this project.”

He added, “Kasiya is not simply a mining project. It is a globally strategic asset.”

The Bigger Picture

Kasiya arrives at a time when global supply chains are being reshaped.

From electric vehicles to defence systems, demand for critical minerals is accelerating, while supply remains concentrated.

Projects that can deliver scale, low cost, and geopolitical alignment are increasingly valuable.

Sovereign Metals appears to be ticking all three boxes.

What is your take on this story?

This is user sentiment & not financial advice.

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.