From Underdog to Must-Have: Why Antimony Is the Hot Ticket in Critical Metals

Key Highlights

- Antimony is a critical metal used in everything from ammunition and batteries to solar panels.

- China’s export ban is tightening global supply, pushing prices to historic highs.

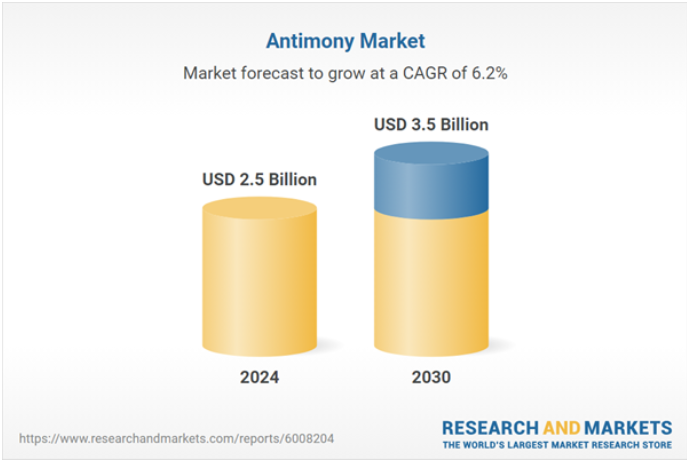

- Global demand for antimony is expected to grow from $2.5 billion in 2024 to $3.5 billion by 2030, at a CAGR of 6.2%.

- Australia, Canada, and the U.S. are ramping up antimony mining projects to reduce dependence on China.

- Several listed companies are advancing gold-antimony projects; near-term producers could benefit from the current market crunch.

- Investors can gain antimony exposure through mining stocks, given there’s no mainstream futures market or ETF for this metal.

Antimony might not grab headlines like lithium or copper, but its time in the spotlight seems overdue. A recent Chinese export ban is poised to push antimony prices beyond even the lofty peaks seen in late 2024, sending shockwaves through industries that rely heavily on this metal. While we can’t confirm if the surge in some antimony-focused stocks stems entirely from this new dynamic, the timing appears more than coincidental.

What is Antimony and Why the Price is Going Up

Source: Pixabay, Picture Description: Antimony semimetal, chemical experiments with antimony in the laboratory.

Market Snapshot

Antimony is a metalloid crucial for flame retardants, solar panels, ammunition primers, and lead-acid batteries. China, which has historically supplied nearly half of the world’s antimony, has now tightened its export curbs, mirroring its restrictions on gallium, germanium, and other critical minerals.

Such moves come at a time when environmental regulations in top producing regions have slowed output and when demand is climbing fast for renewable energy applications (like solar technologies) and defense needs (over 200 types of U.S. Department of Defense ammunition contain antimony). The upshot? A supply squeeze — especially outside China — and soaring prices.

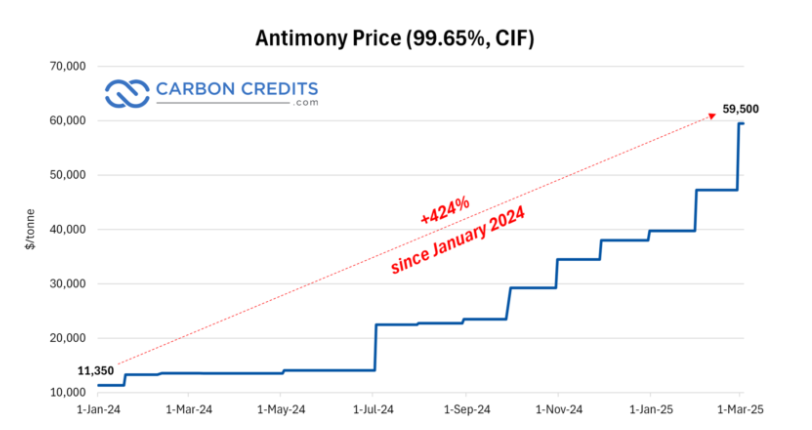

Industry sources suggest antimony traded as high as US$40,000/ton in December 2024, up nearly 250% from earlier that year. Some traders expect US$50,000/ton or even higher in 2025, driven by demand from both the defense and green-energy sectors.

Antimony Price Chart | Source: Carbon Credits & S&P Global

Key Uses of Antimony Across Industries

Antimony’s unique properties make it integral to multiple sectors. Its ability to harden lead, retard flames, and enhance semiconductor performance underpins many critical applications:

Defense: Used in armor-piercing ammunition and bullets (antimony hardens lead for higher penetration), in explosives and ammunition primers, and in military electronics such as night vision goggles and infrared lenses. Antimony trisulfide is a key ingredient in propellants and tracer rounds, making it essential for munitions. These defense uses have become increasingly important as global military activity rises, highlighting antimony as a strategic material for national security.

Energy Storage (Batteries): A vital component in lead-acid batteries, antimony is alloyed with lead to improve battery durability and performance. Nearly all car batteries and many industrial batteries historically used antimony-lead alloys, though some modern designs use calcium as an alternative. Antimony is also at the heart of emerging battery tech: liquid metal batteries for grid storage use molten antimony as one electrode, leveraging its high energy density and stability. As the world builds more renewable energy capacity (which needs storage for when sun or wind are down), antimony-bearing batteries are poised to play a greater role.

Electronics & Semiconductors: Important for semiconductor manufacturing and electronic components. Antimony is used as a dopant in silicon wafers and in compound semiconductors (e.g. indium antimonide and gallium antimonide) for infrared sensors and diodes. It’s also present in solder and alloys for electronics. Furthermore, antimony’s flame-retardant properties protect electronic devices – many plastic casings, circuit boards, and cable coatings include antimony trioxide to meet fire safety standards. In short, antimony helps ensure electronics are both high-performing and fire-safe.

Industrial Materials (Flame Retardants, Glass, Alloys): Antimony trioxide is widely used as a flame retardant additive in plastics, textiles, and rubber, making materials safer in applications from children’s clothing to aircraft interiors. It is also a glass clarifier – small amounts of antimony improve the clarity of optical glass and screens by removing bubbles. In metallurgy, antimony is alloyed with lead and other metals to increase hardness and strength (used in products like bearings, solders, and old typeface printing metals). These industrial uses, while traditional, represent a significant portion of antimony demand and underline its role in everyday products and infrastructure.

China’s Export Ban: A Supply Chain Nightmare

China’s decision to restrict antimony exports—alongside gallium and germanium—has added pressure on already fragile supply chains.

- In 2023, China produced 40,000 tons of antimony, down from 60,000 tons in 2022, due to mine closures and stricter environmental policies.

- Hunan and Guizhou provinces—China’s key antimony-producing regions—have faced industrial accidents and government-imposed mining restrictions, further reducing output.

- Russia and Myanmar, the second and third-largest antimony producers, have also seen disruptions, tightening global supply even further.

With no immediate replacement for Chinese supply, the West is now forced to turn to alternative producers—creating massive investment opportunities for companies developing antimony projects.

Market Trends and Global Demand Surge

Antimony demand is projected to increase from $2.5 billion in 2024 to $3.5 billion by 2030, growing at a CAGR of 6.2%, according to Research and Markets. In the U.S. alone, the antimony market is expected to reach $106.57 million by 2032, driven primarily by OSHA-regulated flame-retardant clothing and expanding use in lead-acid batteries, electronics, and plastics.

According to Fortune Business Insights, Asia-Pacific dominates the global antimony market, accounting for 64.36% of global demand in 2023. The region’s booming automotive and electronics industries are fueling the need for antimony-based flame retardants and alloys.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

North America and Europe, which together account for over 40% of global antimony demand, remain highly dependent on imports from China and India. The growing need for lead-acid batteries, flame retardants, and semiconductors is expected to drive further demand, increasing pressure on global supply chains.

Source: Research and Markets

How to Invest in Antimony

Unlike gold or copper, antimony doesn’t enjoy a robust futures market or popular exchange-traded fund (ETF). So, investors looking to ride the wave generally turn to mining equities. With China tightening its grip on exports, several companies are working to develop antimony projects across Australia, North America, and Europe.

Key Companies Advancing Antimony Projects

- Krakatoa Resources Ltd (ASX: KTA) – Recently acquired the Zopkhito antimony-gold project in Georgia, which hosts an estimated 26,000 tonnes of contained antimony and 815,000 ounces of gold. KTA is advancing the project towards drilling and a Preliminary Economic Assessment (PEA) in the coming year, positioning itself as a key player in the critical minerals sector.

- Antilles Gold (ASX: AAU) – Developing the La Demajagua gold-antimony project in Cuba, expected to start production in Q3 2025.

- Larvotto Resources (ASX: LRV) – Advancing the Hillgrove Gold-Antimony Project in New South Wales, which could supply 7% of global antimony demand.

- Military Metals (CSE: MILI) – Focused on the Trojarova antimony-gold project in Slovakia and the West Gore project in Canada.

- Mandalay Resources (TSX: MND) – Operates Australia’s only significant producing antimony mine, the Costerfield Gold-Antimony Mine in Victoria.

- Nagambie Resources (ASX: NAG) – Developing the Nagambie Gold-Antimony Project in Victoria, Australia.

- Perpetua Resources (TSX: PPTA, NASDAQ: PPTA) – Backed by the U.S. government, working to restart the Stibnite Gold-Antimony Project in Idaho under the Defense Production Act.

- Siren Gold (ASX: SNG) – Exploring New Zealand’s Reefton Gold-Antimony Field, estimated to hold 5% of global antimony reserves.

- Southern Cross Gold (ASX: SXG) – Advancing the Sunday Creek gold-antimony project in Victoria, Australia.

- Trigg Minerals (ASX: TMG) – Holds the Wild Cattle Creek Antimony Project in New South Wales, one of Australia’s highest-grade undeveloped antimony projects.

- United States Antimony Corp (NYSE: UAMY) – The only major antimony refiner in the U.S., with processing facilities in Montana and Mexico.

Global Market Impacts of Soaring Antimony Prices

Antimony’s price surge has rocked global supply chains, leading to both immediate disruptions and long-term strategy shifts. Manufacturers reliant on antimony face skyrocketing costs and difficulty securing material. Sectors like flame retardants, batteries, and defense munitions are particularly affected, raising concerns about production slowdowns and national security.

In response, many buyers are diversifying suppliers beyond China, tapping regions like Tajikistan, Vietnam, and Myanmar. Some companies are even altering processes to produce different antimony compounds or adopting substitutes where feasible. Meanwhile, high prices are driving new investments in antimony mining and refining, including government-backed efforts in the U.S. and projects in Canada and Australia. Though these ventures promise eventual relief, they face long permitting times and won’t solve near-term shortages.

Industries are also testing alternatives—such as lead-calcium alloys in place of lead-antimony batteries or different flame retardant chemistries—to reduce reliance on the metal. Over the long run, experts predict sustained tightness and volatility, prompting manufacturers and governments to forge strategic partnerships and stockpile resources. Whether it’s in defense, energy storage, or everyday products, antimony’s critical role ensures that price and supply challenges will remain front and center for years to come.

What is your take on this story?

This is user sentiment & not financial advice.

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.