Life360 (ASX: 360) hits record Q4 user growth, lifts 2025 outlook as subscriptions keep compounding

Key Highlights

- Record quarter for growth: Monthly active users rose to 95.8 million in Q4 2025, the biggest Q4 net adds in the company’s history.

- Subscriptions keep building: Paying Circles reached 2.8 million, with 576,000 net adds in 2025, a record annual result.

- Guidance upgraded: Life360 now expects FY2025 revenue of US$486 to US$489 million and adjusted EBITDA of US$87 to US$92 million, above prior guidance.

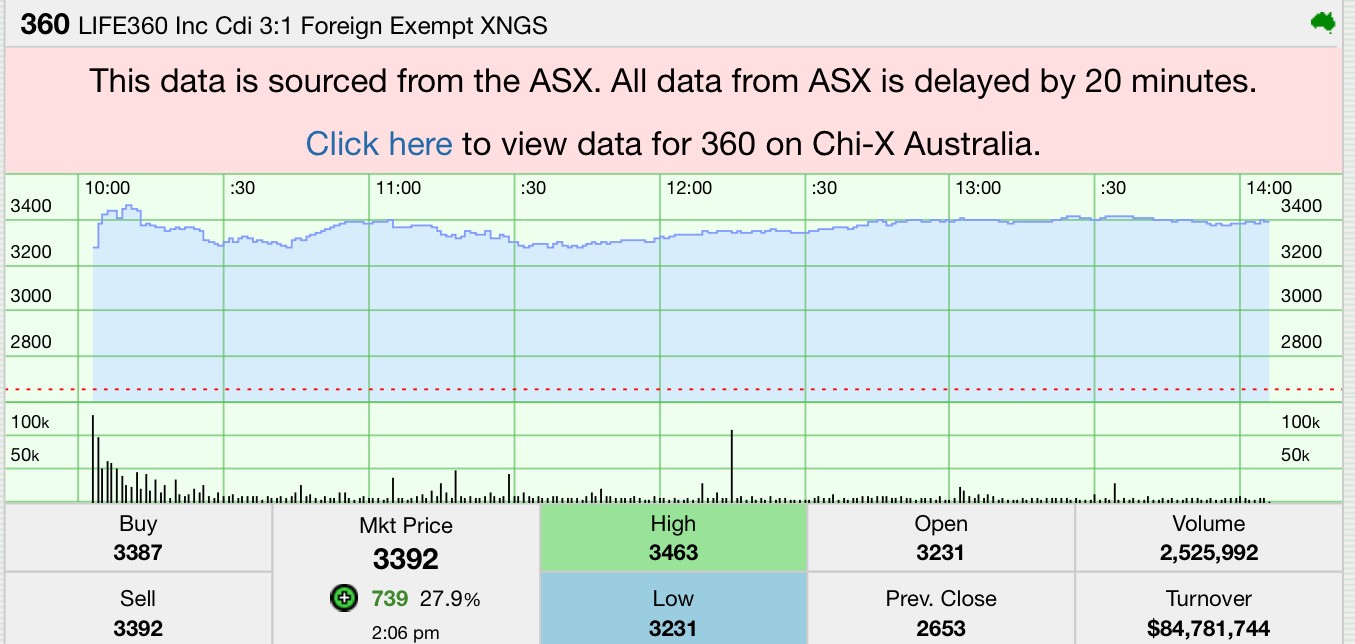

- Market reaction: On the ASX, Life360 shares were up 27.25% to $33.76 in early afternoon trade, with heavy volume. (Price data provided)

Life360 (ASX: 360) has delivered the kind of update growth investors love to see: the user base is rising, more of those users are converting into paying subscribers, and management now expects the year just ended to come in ahead of its own guidance.

In an ASX release today, the family safety and location app maker said Q4 2025 monthly active users climbed to 95.8 million, marking the strongest fourth quarter user growth in its history. Paying Circles, Life360’s core subscription metric, hit 2.8 million in the quarter, while full year 2025 net additions reached 576,000, also a record.

Life360 shares on the ASX traded sharply higher, up 27.25% to $33.76 by 1:58pm AEDT, with 2.49 million shares changing hands (price data provided). That jump fits the tone of the update: momentum appears to be widening rather than fading.

Source: Stocknessmonster

The story behind the numbers: growth, then better quality growth

Life360’s growth engine is running on two tracks: adding users, then converting a portion into paying households.

On users, the company split the quarter cleanly between its home market and the rest of the world:

- US MAU: 50.6 million in Q4 2025, up 1.8 million in the quarter and 16% year over year.

- International MAU: 45.3 million, up 2.4 million in the quarter and 26% year over year.

That second line matters. It suggests Life360 is not relying solely on the US for growth, and it hints that the product’s “family safety” pitch is traveling well across markets, even as consumer apps fight for attention and subscription fatigue becomes a real thing.

On paying users, the company reported:

- Total Paying Circles: 2.8 million in Q4 2025.

- US Paying Circles: 2.0 million, up 23% year over year.

- International Paying Circles: 0.8 million, up 32% year over year.

Subscription growth is not just holding up, it is accelerating in key places. The international Paying Circles growth rate is particularly notable because it implies monetisation is improving outside the US, where pricing, payment behaviour, and local competition can be tougher.

CEO’s take: “the quality of our growth continues to improve”

Management’s language was upbeat but specific, focusing on conversion and consistency rather than hype.

Life360 CEO Lauren Antonoff said:

“Life360 continues to deliver strong, consistent growth across both our user base and paid subscriber base. Q4 2025 represents our strongest operational performance in company history, with record user additions and record subscriber growth. The quality of our growth continues to improve, with newly acquired users converting to paid subscribers at record rates. While we typically see variation quarter-to-quarter, our Q4 2025 and full year 2025 results demonstrate that our growth trends remain intact and consistent, a reflection of the value families place on staying connected and safe. As we look to 2026, we expect overall MAU growth of approximately 20%. As previously indicated, we plan to invest in strategic growth initiatives, while continuing on the path to expand AEBITDA margins.”

There are two phrases worth circling.

First: “converting to paid subscribers at record rates.” Life360 is effectively saying the users it is acquiring now are better matched to the subscription product, whether because marketing is sharper, onboarding is smoother, or the bundle of features is getting clearer.

Second: “invest… while continuing… to expand AEBITDA margins.” That is the balancing act growth investors want to hear about: still spending to grow, but with a plan to keep improving profitability at the same time.

The upgraded outlook: revenue and EBITDA move higher

Life360’s preliminary unaudited numbers point to a stronger finish to 2025 than it previously guided.

The company now expects:

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

- FY2025 revenue: US$486 to US$489 million, about 31% to 32% year over year growth.

- FY2025 adjusted EBITDA: US$87 to US$92 million, implying an 18% to 19% margin.

Those are meaningful margins for a consumer subscription business that is still scaling internationally. It also provides a counterpoint to the common bear case on app-based companies: that growth can be bought, but profitability is harder. Life360 is arguing it can do both, at least at this stage of its curve.

Why the market cared today

A stock does not jump more than 25% on a quiet “we did fine” update. This move looks tied to three things in the release.

- Record operating metrics with breadth

Record MAU additions and record subscriber net adds are straightforward signals. But the geographic split matters too: the international side is not just adding users, it is adding paying households at a faster rate than the US.

- Guidance moved up, not just reaffirmed

The company did not simply restate its earlier targets. It said revenue and adjusted EBITDA will exceed prior guidance, which tends to change the tone of valuation discussions quickly.

- A clear, simple 2026 headline

“Expect 2026 MAU growth of 20%.” It is a clean number that helps the market frame next year’s trajectory, even before the full results and detailed guidance arrive in March.

What to watch next: March results and the cost of growth

Life360 said it will provide comprehensive 2025 results and detailed 2026 guidance on March 2, 2026 (PT) / March 3, 2026 (AEDT), including an investor conference call with the CEO and CFO.

Between now and then, there are a few natural questions the market will likely press:

- How durable are conversion gains? “Record conversion rates” can sometimes reflect a particularly strong cohort or a promotional push. The detail in March will matter.

- Where is the next leg of monetisation coming from? The company references a broader product ecosystem that includes Tile tracking devices and a pet tracker, which can widen revenue streams and deepen retention.

- How heavy will 2026 investment be? Management flagged continued investment in growth initiatives while expanding adjusted EBITDA margins. The mix between marketing, product, and international expansion will shape the year.

Stock snapshot (ASX: 360)

Based on the trading data provided:

- Last: $33.76, up $7.23 (27.25%)

- Volume: 2,485,284 shares

- Market cap: $8.01 billion

- 52-week range: $14.93 to $55.87

- 1-year return: 36.07%

The bigger picture

Life360’s update reads like a company that is still in expansion mode, but increasingly focused on turning scale into a more predictable earnings profile. The headline numbers are strong, but the more important message is underneath them: user growth is broad-based, subscription growth is compounding, and profitability is moving in the right direction, even as the company keeps spending to build.

That combination is not common, which is why the market moved first and asked questions later.

What is your take on this story?

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.