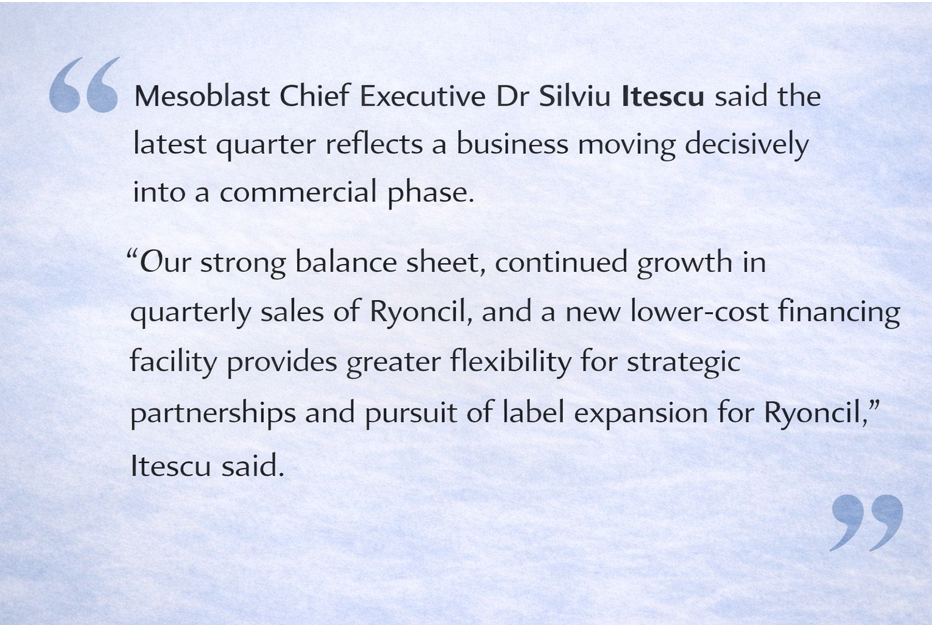

Mesoblast Surges as Ryoncil Sales Jump 60%, Strengthening Balance Sheet and Commercial Momentum

Team Skrill Network

Team Skrill Network comprises seasoned professionals from diverse fields including Finance, Mining, Technology, Investing, and Digital Strategy. They bring a deep knowledge and understanding of financial markets and behavioural patterns to every story, ensuring credibility and precision in every piece. Whether analysing emerging market trends or spotlighting small- and mid-cap growth companies across ASX, TSX, or NASDAQ, the team’s editorial approach blends data-driven insights with compelling storytelling. Their expertise enables them to process complex developments into content that resonates with both institutional investors and retail audiences. Backed by experience in content curation, SEO strategy, and investor-focused messaging, the team of writers at Skrill Network are committed to delivering stories that matter—authentic, relevant, and strategically aligned with the evolving landscape of global investing.

Read more

Key Highlights

- Ryoncil sales rose 60% quarter-on-quarter to US$35.1 million

- First FDA-approved MSC therapy continues to scale in the US market

- New US$125 million facility strengthens balance sheet flexibility

- Adult trial expansion opens a significantly larger addressable market

Mesoblast Ltd has kicked off 2026 with renewed momentum, as the ASX-listed biotechnology company delivered a sharp increase in commercial revenue and reinforced its financial position. The company’s latest update shows accelerating traction for its flagship cell therapy Ryoncil, alongside balance sheet improvements that could reshape its strategic options over the coming year.

At midday trade on Friday, Mesoblast shares were up 9.15% at $3.22, hovering near the top of their 52-week range of $1.515 to $3.31. The company now carries a market capitalisation of approximately $4.13 billion, reflecting growing confidence in its commercial transition.

Ryoncil Sales Gain Real Momentum

The standout development in Mesoblast’s update was a 60% quarter-on-quarter increase in Ryoncil sales, which reached US$35.1 million for the December 2025 quarter. The result marks a clear inflection point for the company, which has spent more than a decade developing its allogeneic cell therapy platform.

Market Snapshot

Ryoncil, known scientifically as remestemcel-L-rknd, is currently approved by the US Food and Drug Administration for the treatment of steroid-refractory acute graft-versus-host disease in children under the age of 12. It remains the only FDA-approved mesenchymal stromal cell therapy for any indication.

The revenue growth reflects deeper penetration into US pediatric transplant centres and improved supply chain execution following FDA approval.

Source: Mesoblast Limited ASX announcement

Adult Indication Expansion Changes the Scale

Beyond the current pediatric market, Mesoblast confirmed that Ryoncil will now be evaluated in a pivotal trial as part of a second-line treatment for adults with steroid-refractory acute graft-versus-host disease.

This is a meaningful step change. According to the company, the adult market is approximately three times larger than the pediatric segment, potentially transforming Ryoncil from a niche therapy into a far broader commercial product.

For newer market participants, graft-versus-host disease is a serious and often fatal complication following bone marrow transplants, where donor immune cells attack the patient’s tissues. Steroid-resistant cases have limited treatment options, making this a high-need therapeutic area.

If successful, adult approval could materially lift Mesoblast’s long-term revenue trajectory and strengthen its negotiating position with potential partners.

Balance Sheet Reset Lowers Financial Risk

Mesoblast also used the update to outline significant improvements to its balance sheet structure. The company recently secured a new US$125 million five-year interest-only facility from its largest shareholder.

The facility replaces higher-cost legacy debt and allows Mesoblast to repay its previous senior secured loan in full. Importantly, the new financing carries no exit fees, no early repayment penalties, and does not encumber the company’s core intellectual property.

The facility also enables partial repayment of a subordinated royalty facility, which management expects to be fully retired by mid-calendar 2026 through ongoing revenue generation.

From a strategic standpoint, the cleaner balance sheet gives Mesoblast greater freedom to pursue licensing deals, co-commercialisation partnerships, or further clinical expansion without near-term funding pressure.

Why This Matters for the Broader Biotech Sector

Mesoblast’s update comes at a time when global biotech markets remain selective. While early-stage development stories have struggled, companies with approved products and visible revenue growth have increasingly stood out.

Ryoncil’s commercial performance places Mesoblast in a relatively rare category among Australian-listed biotech companies: one with FDA approval, growing US revenues, and late-stage pipeline expansion already underway.

The company’s proprietary manufacturing process also underpins its scalability. Mesoblast produces industrial-scale, cryopreserved, off-the-shelf cellular medicines that can be distributed globally with pharmaceutical-grade consistency.

This manufacturing capability is often overlooked, but it represents a critical barrier to entry in the cell therapy space.

Intellectual Property Provides Long-Term Protection

Mesoblast holds a substantial global intellectual property portfolio, with more than 1,000 granted patents and pending applications covering cell compositions, manufacturing methods, and therapeutic indications.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

According to the company, these protections extend through to at least 2044 across major markets, providing long-term commercial defensibility for both Ryoncil and its broader pipeline.

In addition to graft-versus-host disease, Mesoblast continues to develop therapies for inflammatory bowel disease, heart failure, and chronic low back pain using its remestemcel-L and rexlemestrocel-L platforms.

Market Context and Share Price Performance

From a market perspective, Mesoblast’s 1-year return of 14.59% reflects steady recovery following volatility earlier in the biotech cycle. Trading volumes were elevated on Friday, with more than 10.8 million shares changing hands by early afternoon.

The stock’s move higher aligns with renewed interest in healthcare names showing real-world revenue growth, rather than purely clinical milestones.

While the company remains loss-making on a net basis, the rising contribution from Ryoncil sales continues to narrow the gap toward operational sustainability.

Looking Ahead

The next 12 months will likely centre on three key themes for Mesoblast. First, continued growth in pediatric Ryoncil sales across the US. Second, progress on adult clinical trials that could unlock a much larger market. Third, strategic execution enabled by a strengthened balance sheet.

With regulatory risk largely behind it for its lead asset, Mesoblast now faces the execution challenge of scaling manufacturing, market access, and clinical expansion in parallel.

For a sector often defined by promise rather than performance, Mesoblast’s latest update shows a company increasingly defined by delivery.

What is your take on this story?

This is user sentiment & not financial advice.

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.