Weekly Wrap: ASX Edges Lower as Tech Leadership Shifts and Banks Face Fresh Pressure

Team Skrill Network

Team Skrill Network comprises seasoned professionals from diverse fields including Finance, Mining, Technology, Investing, and Digital Strategy. They bring a deep knowledge and understanding of financial markets and behavioural patterns to every story, ensuring credibility and precision in every piece. Whether analysing emerging market trends or spotlighting small- and mid-cap growth companies across ASX, TSX, or NASDAQ, the team’s editorial approach blends data-driven insights with compelling storytelling. Their expertise enables them to process complex developments into content that resonates with both institutional investors and retail audiences. Backed by experience in content curation, SEO strategy, and investor-focused messaging, the team of writers at Skrill Network are committed to delivering stories that matter—authentic, relevant, and strategically aligned with the evolving landscape of global investing.

Read more

Key Highlights

• ASX 200 edges 0.22% lowet by Friday midday facing a volatile trading week.

• Domestic technology stocks rebound while Wall Street’s “Magnificent 7” lose momentum.

• Banking shares remain under pressure after Judo Capital’s earnings downgrade.

Market Snapshot

• Investors weigh slowing economic growth against resilient employment and persistent inflation.

The Australian share market is heading into the final trading session of June with modest gains, but the week has highlighted just how quickly market leadership can change.

By Friday midday, the S&P/ASX 200 edged lower by 0.22% to 8,729.5 points, observing a week that swung between optimism over easing inflation, renewed pressure on banks and shifting global sentiment around technology stocks.

The broader picture was less about dramatic index moves and more about rotation. Investors moved capital between sectors as they weighed cooling inflation, resilient employment, softer commodity prices and growing questions over whether Wall Street’s artificial intelligence leaders can continue delivering the growth markets have come to expect.

The week’s biggest talking point remained the changing mood surrounding the so called “Magnificent 7” technology giants in the United States.

While the Nasdaq still finished higher overnight, many investors are beginning to question whether years of heavy spending on artificial intelligence infrastructure can continue without stronger earnings growth.

Tony Sycamore, market analyst at IG, said the market is beginning to broaden beyond the largest technology names.

“Fatigue about the ‘Magnificent 7’ stocks is deepening in the US. The small-cap Russell 2000 is outperforming the Nasdaq 100, up around 21% year-to-date compared with roughly 17% for the tech-heavy index.”

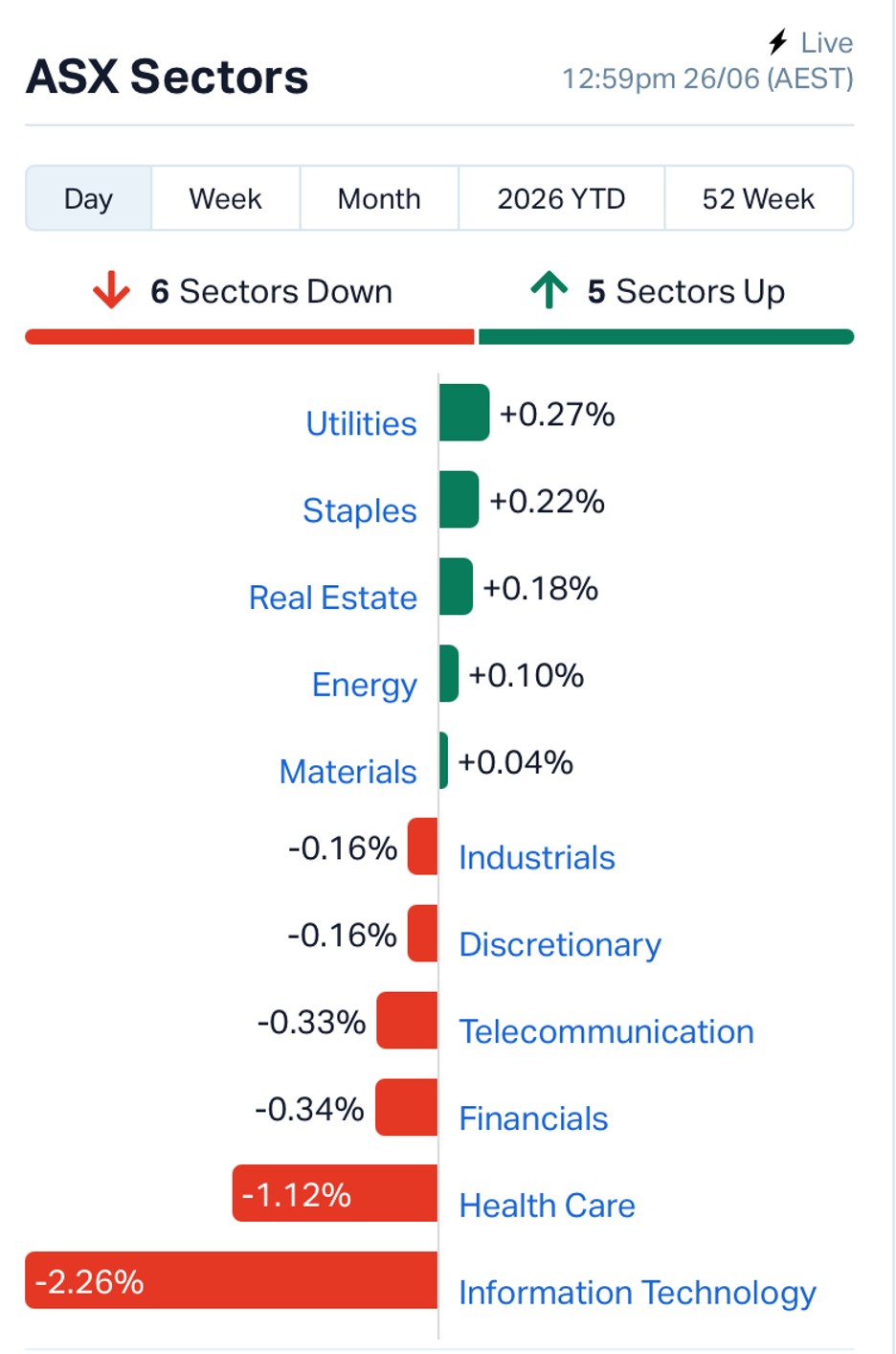

ASX Sector Snapshot | Source: MarketIndex

That shift has not gone unnoticed in Australia. After outperforming earlier in the week, local technology shares gave back some gains on Friday, with the S&P/ASX All Technology Index falling 2.26%. Healthcare stocks also weakened as money flowed into more defensive sectors.

Materials led the market with a 0.04% gain, supported by renewed buying in selected gold producers despite softer commodity prices. Utilities and consumer staples also attracted buyers seeking stability.

Macro Drivers: Strong Labour Market Meets Slowing Growth

Australian markets finished the week caught between two competing narratives.

On one hand, the latest labour market data continued to highlight the resilience of the domestic economy. Australia’s unemployment rate eased to 4.4%, reinforcing expectations that the jobs market remains tight despite higher interest rates.

On the other hand, economists are becoming increasingly cautious about economic momentum. Westpac expects June quarter GDP growth of just 0.2%, while annual growth is forecast to slow to 1.7%, below the Reserve Bank of Australia’s projections. That combination leaves policymakers balancing a slowing economy against inflation that remains stubbornly above target.

Meanwhile, markets continue to price the possibility that the RBA could keep interest rates higher for longer if underlying inflation fails to ease over coming months.

Adding another layer of uncertainty, regulators also stepped up scrutiny of Australia’s retail sector, with the ACCC preparing tougher supermarket pricing oversight from July 1 following recent court action against Coles over misleading discount pricing.

Global Markets: Investors Rotate Beyond Big Tech

Overseas markets continued to show signs that leadership is broadening beyond the US technology giants.

While the Nasdaq managed to finish higher overnight, investors remain increasingly selective after weeks of volatility across the “Magnificent 7”. Rising AI infrastructure spending has shifted attention from revenue growth to profitability, with markets demanding stronger earnings ahead of the upcoming US reporting season.

IG Market Analyst Tony Sycamore noted that smaller US companies are now outperforming many of the mega-cap technology leaders, highlighting a gradual rotation into broader areas of the market.

At the same time, stronger US Treasury yields and a firmer US dollar continued to pressure commodity prices globally.

Commodities: Broad-Based Weakness Pressures Resources

Commodity markets remained under pressure on Friday, reflecting a stronger US dollar, easing geopolitical tensions in the Middle East and softer global growth expectations.

Source: MarketIndex

Brent crude fell 1.32% to US$74.27 a barrel, while WTI crude declined 1.31% to US$70.98, extending this week’s sharp retreat as traders unwound much of the geopolitical premium that had been built into oil prices.

Precious metals also softened.

Gold slipped 0.86% to US$3,992.65 an ounce, falling back below the psychological US$4,000 level as higher bond yields reduced demand for defensive assets.

Silver experienced heavier selling, dropping 3.17% to US$56.01 an ounce, highlighting the metal’s dual exposure to both precious metals sentiment and industrial demand.

Industrial metals were weaker as well.

Copper eased 1.51% to US$5.98 per pound, reflecting ongoing concerns over global manufacturing activity and slower demand from China, despite the longer-term outlook remaining supported by electrification, renewable energy investment and AI-related infrastructure.

The broad decline across energy, precious metals and base metals weighed on parts of the Australian resources sector, although selective gold producers continued to attract buyers on company-specific catalysts.

Adding another layer to the week’s developments, the Australian Competition and Consumer Commission announced tougher oversight of supermarket pricing from July 1. The move follows a Federal Court ruling that Coles misled consumers over discount pricing and signals increased regulatory scrutiny across Australia’s major retailers.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

Financial stocks endured one of their toughest weeks in months after Judo Capital shocked the market with a sharp downgrade to its earnings outlook.

The lender slashed its FY26 profit guidance after increasing provisions for bad and doubtful debts, triggering a sharp sell-off that spread across the broader banking sector.

Although Australia’s major banks remain well capitalised, the episode reignited concerns about elevated valuations.

Morningstar market strategist Lochlan Halloway noted that roughly A$11 billion has now been positioned against the major banks through short selling.

“Sure, it’s a large number, but it’s only 2% of the four majors’ combined market cap of some A$620 billion. The vast majority of investors are still long the banks.”

He added that historically, elevated short interest has not consistently translated into sustained share price declines, suggesting markets may already be pricing in many of the sector’s risks.

Among individual stocks, Solstice Minerals jumped more than 30% to lead the market, while Brightstar Resources and Resolute Mining also advanced as gold explorers attracted renewed interest.

James Hardie, which rallied strongly earlier in the week, remained among the better performing industrial names.

On the downside, Clarity Pharmaceuticals, DroneShield and CAR Group all retreated following recent strong gains, reflecting continued profit taking across higher growth companies.

Beyond daily market movements, another structural trend emerged this week.

New research from the Super Members Council found advice fees deducted from superannuation accounts have increased by A$1.1 billion over the past two years. Separate research from the Association of Superannuation Funds of Australia showed younger Australians are increasingly turning to social media for retirement guidance as professional financial advice becomes more expensive and less accessible.

Taken together, the week’s developments point to a market searching for its next source of leadership.

Technology remains central to long-term growth, but investors are becoming increasingly selective. Banks face closer scrutiny following Judo Capital’s surprise downgrade, while miners continue to benefit from long-term demand linked to electrification, critical minerals and gold’s defensive appeal.

As June draws to a close, Australia’s share market appears to be balancing resilient corporate earnings against slower economic growth, persistent inflation and changing global investment themes. Rather than chasing a single narrative, investors are increasingly rewarding companies with stronger balance sheets, clearer earnings visibility and disciplined execution.

Sources: Australian Bureau of Statistics (ABS), Reserve Bank of Australia (RBA), Westpac Economics, IG Markets, Morningstar, ACCC, Super Members Council, Association of Superannuation Funds of Australia (ASFA), company announcements and ASX market data.

What is your take on this story?

This is user sentiment & not financial advice.

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.